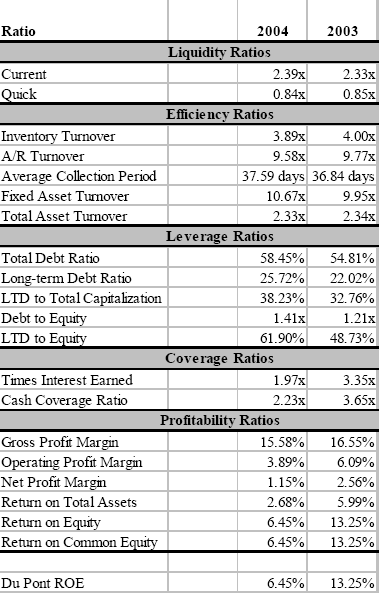

Obviously, ROYAL BALI CEMERLANG’s profitability has slipped rather dramatically in the past year. The sources of these declines can be seen most clearly if we look at all of ROYAL BALI CEMERLANG’s ratios.

The gross profit margin in 2004 is lower than in 2003, but not significantly (at least compared to the declines in the other ratios).

The operating profit margin, however, is significantly lower in 2004 than in 2003. This indicates potential problems in controlling the firm’s operating expenses, particularly selling, general, and administrative expenses. The other profitability ratios are lower than in 2003 partly because of the “trickle down” effect of the increase in operating expenses. However, they are also lower because ROYAL BALI CEMERLANG has taken on a lot of extra debt in 2004, resulting in interest expense increasing faster than sales. This can be confirmed by examining ROYAL BALI CEMERLANG’s common-size income statement.

Finally, the Du Pont analysis of the firm’s ROE has shown us that it could be improved by any of the following:

- Increasing the net profit margin

- Increasing the total asset turnover; or

- Increasing the amount of debt relative to equity

Our ratio analysis has shown that operating expenses have grown considerably, leading to the decline in the net profit margin. Reducing these expenses should be the primary objective of management.

Since the total asset turnover ratio is near the industry average, as we’ll soon see, it may be difficult to increase this ratio. However, the firm’s inventory turnover ratio is considerably below the industry average and inventory control may provide one method of improving the total asset turnover. An increase in debt is not called for, since the firm already has somewhat more debt than the industry average.

Source:

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.